Final Loan Approval and Closing Prep: What Happens After You’re Under Contract?

So now we’re starting to get down to the nitty gritty, and we’re going to work on getting you to the finish line.

Once you go under contract, that means you’re fully executed, it’s time for all the players in the game to start working on their parts. My job is to oversee the whole process and help make sure everything gets done as smoothly as possible. This is where I shine, because I love working with everyone in a way that is as a team to get you into your dream home.

Once we’re under contract, we’re going to start scheduling inspections because the 10-day due diligence period has begun.

You’ll also make your official loan application with the lender. You’ve probably already started this process during pre-approval, but now it’s the formal application tied to the specific property you’re buying.

At this point, you’ll typically pay for the appraisal, although the appraisal usually doesn’t happen right away.

You’ll also wire your escrow deposit, sometimes called a binder deposit, to the title company.

Behind the scenes, several things are happening at the same time. The lender is beginning their process, the title company is opening escrow and starting their work, and the inspection period is underway.

Here’s more information on the Inspections and appraisal process in my first time home buyer series.

After The Inspections and Repairs

Now, let’s say everything goes well with the inspections. Whether you decide to move forward with the home as-is or there are repairs that the seller agrees to make, the process keeps moving forward.

If repairs are negotiated, the seller will start working on those as well.

Once we get through the 10-day due diligence period and you’ve completed your inspections, the next major step is the appraisal.

After you pay for the appraisal, the lender will order it. An appraiser will come out to the property and take photos, measure the house, and gather information about the home, including any upgrades or improvements that have been made.

They’ll also review comparable homes that have recently sold, along with homes that are currently active and pending in the area. The appraisal process itself usually doesn’t take very long. Many times it’s under a week.

Once the appraisal is completed, we’ll hear back from the lender regarding the appraised value of the property.

If the home appraises at or above the contract price, we’re good to go and can continue moving forward toward closing.

If the appraisal comes in lower than the contract price, we may need to negotiate with the seller. In many cases, we’ll ask if they’re willing to lower their price to match the appraised value. Depending on the type of market we’re in, it’s fairly common for sellers to agree to that.

Appraisal Is Complete and Good….

During this time, your lender is going to be asking you for paperwork, so make sure you’re staying on top of any requests they send over. The faster you get documents back to them, the smoother the process usually goes.

Once the house appraises, everything gets sent over to underwriting.

I always joke with my buyers that the underwriters are locked away in a warehouse in a room with no windows, and all they do all day is underwrite loans. They’re not allowed to come out until they finish. Of course, that’s not really true, but it usually gets a laugh.

The underwriter’s job is to review everything and make sure the loan meets all of the lender’s requirements. Sometimes they’ll come back with a list of conditions that need to be cleared before they can give final approval.

Some of those conditions may be related to the appraisal report, depending on what the appraiser noted. Other times they may simply need additional documentation from the buyer.

This is completely normal and usually nothing to worry about. We just need to work through the requests, get the documents turned in, and clear any remaining conditions.

Once the underwriter reviews everything and signs off on the file, you’ll receive one of the most exciting updates in the home buying process: Clear to Close.

At that point, assuming the title work has been completed, the survey has been reviewed if one is required, and everything else is in order, we can move forward with scheduling your final walk through and closing.

A lot of buyers imagine that everyone sits around one big table and signs paperwork together. Sometimes that happens, but not always.

In some transactions, the buyer and seller sign at the same time. In others, the seller signs first or the buyer signs first. Sometimes they may even sign on different days.

Every transaction is a little different depending on the schedules of the buyer, seller, lender, title company, and whether anyone is moving out of the area. The important thing to know is that once you’re clear to close, you’re in the home stretch.

Common Mistakes to Avoid Before Closing

There are a few things that can happen during this process that buyers don’t always understand, and I want to make you aware of them ahead of time.

One of the biggest frustrations buyers have is that it can feel like the lender keeps asking for the same documents over and over again. It happens more often than you’d think.

To make things easier, I recommend creating a folder on your computer where you keep all of your loan documents. Store your pay stubs, W-2s, bank statements, tax returns, and any other paperwork the lender may request. That way, when they ask for something, you can find it quickly and send it over.

You want to stay on top of these requests, because delays in getting documents back to the lender can slow down your closing. In some cases, it could even affect your loan approval if required documents aren’t provided.

Another mistake I see buyers make is getting excited and wanting to buy furniture before they close. Get excited, just don’t act on that.

Now, if you’re paying cash for something small, that’s one thing. But if you’re financing furniture, opening a new credit account, or taking on additional debt before closing, that could potentially cause problems with your loan approval.

If your debt-to-income ratio is already close to the lender’s limits, adding a new payment could change your qualification numbers and put the transaction at risk.

I also recommend avoiding large cash purchases before closing. Large deposits and withdrawals can create additional questions from the lender, and you may have to provide documentation explaining where the money came from or where it went.

The safest approach is simple: wait until after closing before making major purchases for your new home. Cash and especially credit.

Another mistake I’ve seen buyers make is changing jobs before closing.

If you know a job change may be coming, talk to your lender before making any decisions. A change in employment can affect your loan approval, depending on the circumstances.

Sometimes it’s not a big issue. For example, if you’re staying in the same line of work and moving to a better-paying position, the lender may be able to work with that. In some cases, they may ask for a letter from the new employer confirming your start date, salary, and other employment details.

Every lender’s requirements can be different, which is why it’s important to communicate with them before making any major financial or employment changes.

When you’re under contract, my advice is simple: don’t make any major financial moves without talking to your lender first. It can save you a lot of stress and help keep your transaction on track.

Not sure what you should or shouldn’t do while you’re under contract?

Before making any major financial decisions, reach out and ask. A quick conversation could help you avoid unnecessary delays or surprises before closing.

Have questions? Don’t be shy or worried you’ll be harassed by a crazy real estate agent. I love answering questions and educating you on the local area, the home buying and selling process, without the pressure!!! Reach out by calling or text: 904-910-3516

Have questions? Don’t be shy or worried you’ll be harassed by a crazy real estate agent. I love answering questions and educating you on the local area, the home buying and selling process, without the pressure!!! Reach out by calling or text: 904-910-3516

Timeline Expectations and What to Expect Next

One thing I want buyers to understand is that once you’re under contract, there can be periods where it feels like nothing is happening.

In reality, a lot is happening behind the scenes.

The lender is reviewing documents, the title company is working on the title search, the appraisal is being completed, inspections are being negotiated, and various parties are coordinating to get everything ready for closing.

Some days you may hear from multiple people asking for documents or signatures. Other days may be completely quiet.

That doesn’t necessarily mean there’s a problem.

A typical contract period is often around 30 to 45 days, although that can vary depending on the type of loan, the lender, and the terms of the contract. Some transactions move faster and some take longer.

My job throughout the process is to help keep everything moving forward, stay in communication with all the parties involved, and help you navigate any bumps in the road that come up along the way.

Before closing, we’ll schedule a final walk through of the property. This gives you an opportunity to make sure the home is in the condition you expect, verify that any agreed-upon repairs have been completed, and confirm that nothing has changed since you last saw the property.

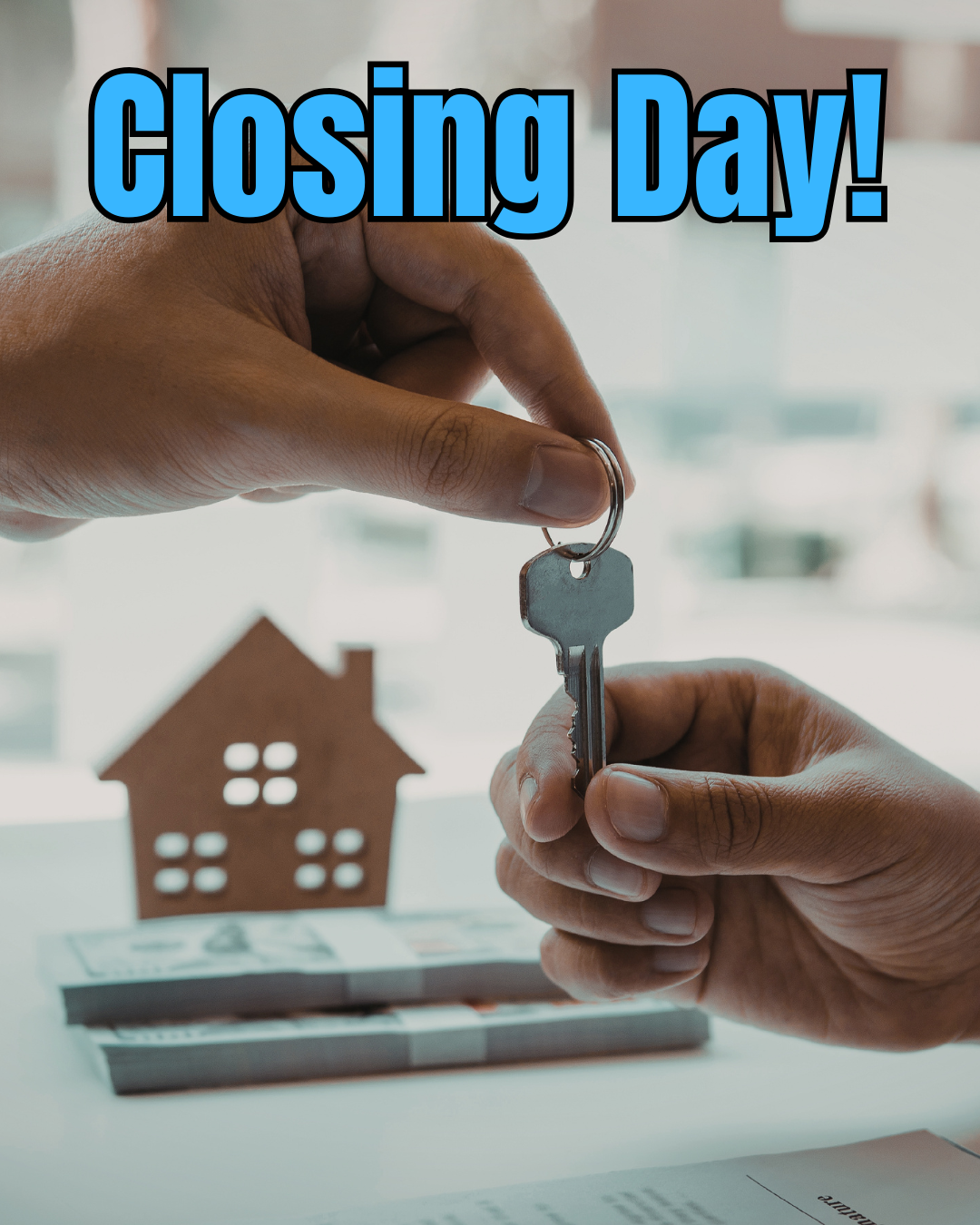

Then comes closing day. The day we’ve been waiting for!!! Woohoo!!!!

You’ll sign what feels like a mountain of paperwork, the funds will be transferred, the deed will be recorded, and once everything is finalized, you’ll get the keys to your new home. Same day, as long as the funding is complete.

Buying a home can feel overwhelming at times, but if you’ve made it this far, you’re almost there. Stay responsive, communicate with your lender, and don’t make any major financial changes before closing. If you do that, you’ll give yourself the best chance of making it to the finish line without any surprises.

Ready to Buy a Home in Northeast Florida?

Buying a home can feel overwhelming, but you don’t have to figure it out alone. If you’re thinking about buying in Jacksonville, Clay County, St. Johns County, or the surrounding Northeast Florida area, let’s talk.

Call, text, or email me with your questions. Even if you’re still months away from buying, I’m happy to help you create a plan and understand your next steps.

Have questions? Don’t be shy or worried you’ll be harassed by a crazy real estate agent. I love answering questions and educating you on the local area, the home buying and selling process, without the pressure!!! Reach out by calling or text: 904-910-3516

Just started the process and need to speak to a lender? Reach out to Deb Frazier with Coast2Coast Mortgage.

I’m Pam Graham, a Northeast Florida real estate consultant, which includes Jacksonville, Clay & St John’s Counties. I break down the market in layman’s terms so you can make smart decisions—whether you’re buying, selling, or just keeping an eye on what’s happening.

Call/Text 904-910-3516

Email: pam@pamgraham.com